2021 announced itself as the year of freedom. Still, we’re writing this blog post from a quarantined home office while a new pandemic wave comes crashing down. Pretty sure this is not what anyone was expecting.

It’s good news, then, that one of the main takeaways from the latest #BelgianGamesIndustry survey report is that our local video gamesector is showing a vigorous amount of resilience. Some key figures* to back that up:

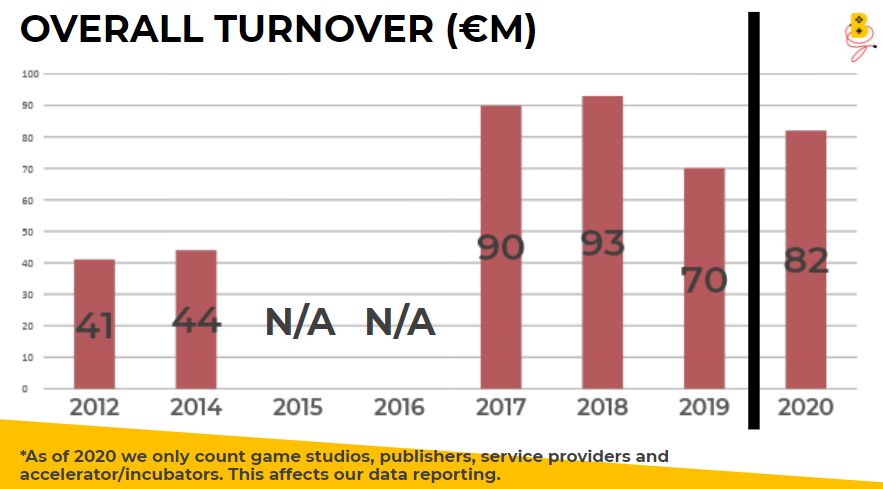

- Compared to 2019, overall turnover went up 17% to €82 million

- 60% of companies expect expect turnover to further rise in 2021

- 47% of companies expect their FTE count to also rise in 2021

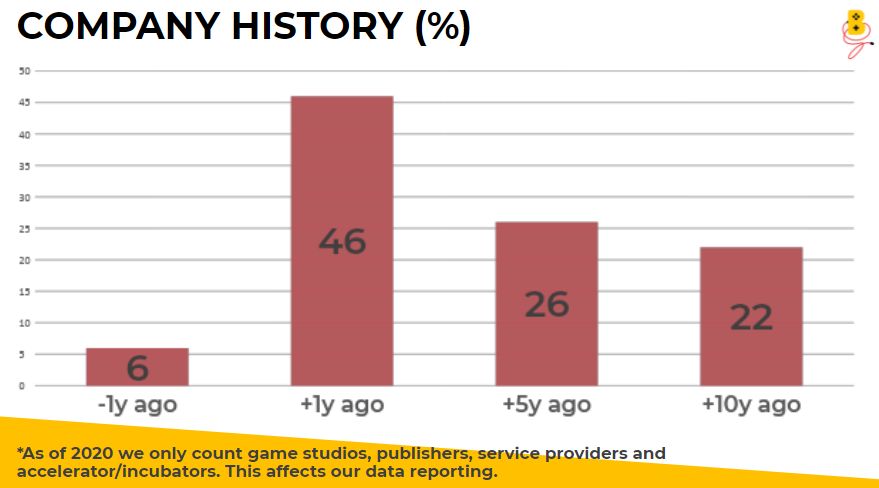

- Almost 50% of active and registered companies are 5 years or older

- Growing demand (63% vs 56% last year) for tax shelter to sustain future projects

Download the full report right here. And read on for more background and insights.

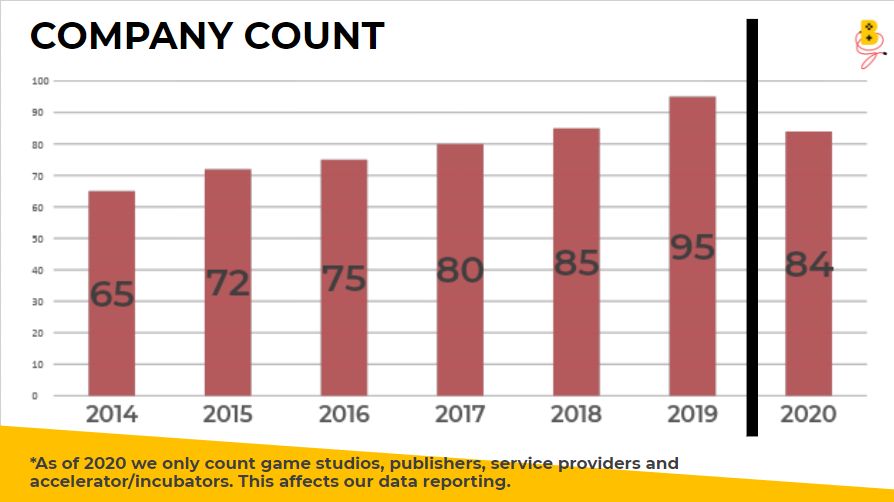

Taking into account the new survey eligibility*, there’s 84 video game studios, publishers, service providers and accelerators/incubators in Belgium. This might look like a drop from last year, but again, the new way of analysing affects the data. Even with “fewer” players in the game, the overall turnover of our ecosystem has gone up with 17%, evening out at a very respectable €82 million. Granted, a big chunk of that is down to the soaring early access release of Baldur’s Gate 3, but there’s more companies who saw a higher turnover than expected.

In terms of geographical spread, there’s not a lot of movement. The majority of Belgian video game companies is still based in Flanders (71%) with the provinces of West Flanders, East Flanders and Antwerp accounting for over half of all companies. Wallonia (20%) and Brussels (9%) remain at a fairly similar level as last year. Remarkably, the province of Hainaut is the only region that managed a significant growth. Video game hot spots like Mons and Charleroi seem to be creating a healthy ecosystem south of the language border as well.

It might be an indication that Brussels and Wallonia will follow a similar growth pattern as Flanders in the next five years, as these regions boast plenty of video game startups working on their first titles. In Flanders, these startups resulted in a massive influx of new players with almost half of our Belgian companies being founded between 1 and 5 years ago. While it’s great that 48% of companies have lived past the 5 year mark, it goes to show that our industry is still fragile, especially when you contemplate 85% of our companies still consist of 10 people max.

Belgian studios are known for their creative output so it’s no wonder that close to 80% of our companies are working on their own IP. Still, almost half of them indicate they have to engage in work for hire to sustain development of their own projects. That’s not necessarily a bad thing, but there’s already ample examples of promising titles that lost momentum and focus because the team had to constantly switch up projects.

In conclusion, there’s plenty to be happy about and there’s more good stuff ahead. With Belgian key releases like Baldur’s Gate 3 (unconfirmed, but likely), Outcast 2, Shredders and You Suck at Parking bound to hit somewhere in 2022, the #BelgianGamesIndustry might be at the edge of its biggest year ever. There’s an evolution here that’s hard to ignore.

David Verbruggen, FLEGA General Manager: “Our sector shows incredible resilience in the face of the covid pandemic, installing robust work from home procedures and achieving turnover growth. We are experiencing a momentum pushing us to new heights, but our ecosystem still is very fragile and we lag far behind neighbouring countries such as France, Germany and UK. For this, we are looking forward to tax shelter and other public support measures, but we also welcome local publishers to set up shop and private investors to pump money into our sector. We aim to be an innovative driver in the Belgian economy and reach out to other sectors looking to work with us.”

With a maturing ecosystem indeed comes a growing demand for structural investments. To keep growing and become even tougher in the wake of future pandemic waves (a very real scenario, unfortunately), there’s a need for more money. Bigger investments can secure a stable future for our developers so they do what they do best: create world class video game experiences.

Hungry for more insights? Download the full report right here.

* Just leave it to good old methodology to complicate matters a bit. In order to get easier comparable results with other European countries, as of 2020 we only count active and registered video game studios, publishers, service providers and accelerators/incubators. As opposed to previous years, this leaves out game departments at non game companies, research programs and educational institutions. This doesn’t always make it easy to draw direct comparisons between previous years, but let’s make this statistical voyage as smooth as possible. Remember that we did never take into account companies only active in esports, retail, media or related services (such as advertising, PR, marketing, legal, HR…).