We’re nearly at the end of this crazy ride called 2020. Before diving into a well deserved yet socially distanced holiday period, we’d like to share some interesting results from the latest #BelgianGamesIndustry survey. Any other year you would’ve heard about this sooner over a nice drink at gamescom, but yeah *gestures* – 2020

Some quick methodology before we start: this survey was conducted from June to September 2020 (between the first and second COVID-19 waves) and aimed at active game developer studios, publishers, game platforms/portals, service providers, schools/educational institutions that offer dedicated game education programs, research departments that study games, and game events, audio, acceleration, incubation companies with offices in Belgium and/or abroad. Participation was opt-in.

According to the survey results, the #BelgianGamesIndustry continues to mature, but the future challenges we identified last year are catching up with us rather quickly. One thing we’re very pleased with is that our local soil still looks fertile enough for a lot of new game companies to surface.

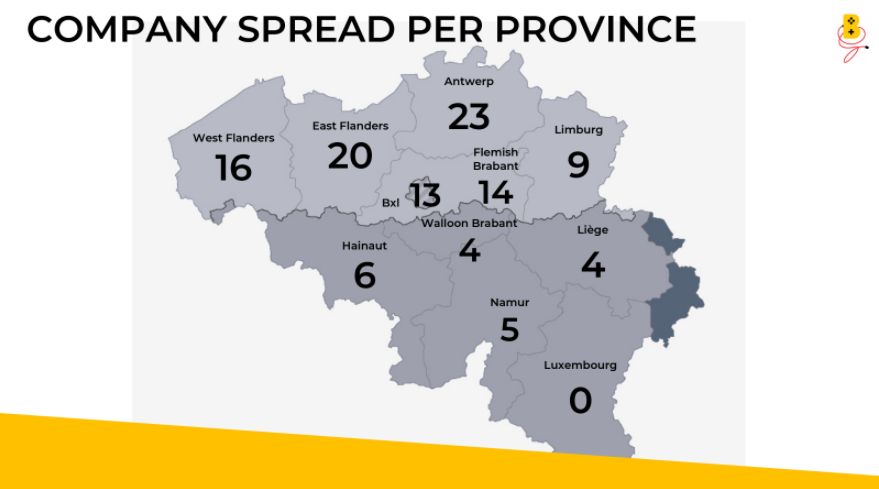

There are now 114 registered active game companies in Belgium, up from 95 last year. With 82 companies, Flanders still makes up for the majority of these, with Wallonia and Brussels featuring 19 and 13 companies respectively. Quick footnote: the Belgian ecosystem also has a lot of very small non-registered entities that are working on their first game and still don’t make any revenue. These entities are not accounted for in our company overview. Half of Belgian game companies are based in West-Flanders, East-Flanders and Antwerp.

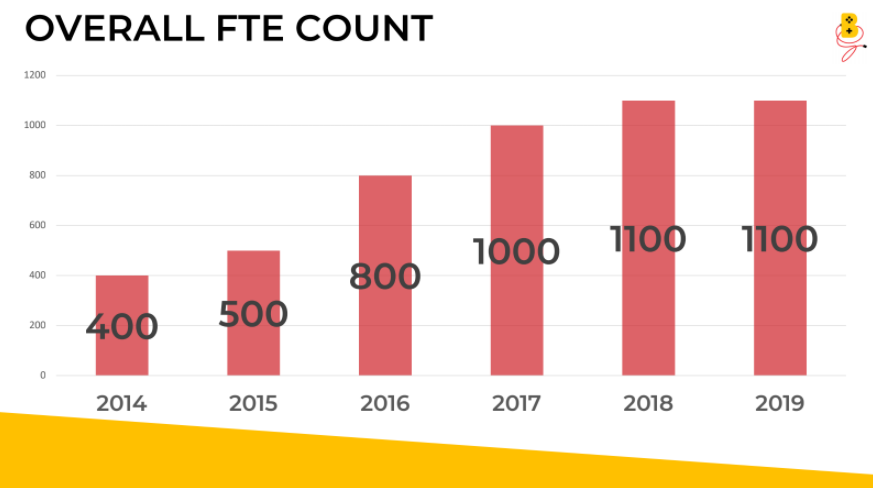

While this proves our local industry is continuing to grow, the number of FTE’s suggests otherwise. Just like last year, 1100 persons are making a living from working in the #BelgianGamesIndustry. Exponential growth of FTE’s has been in decline for some years, but it’s the first time the numbers aren’t moving at all. Our ecosystem still faces a high degree of brain drain from Belgian students to studios abroad or other, more stable industries and it’s beginning to show. Combined with the influx of new companies, this proves more companies are working with fewer full time staff than last year.

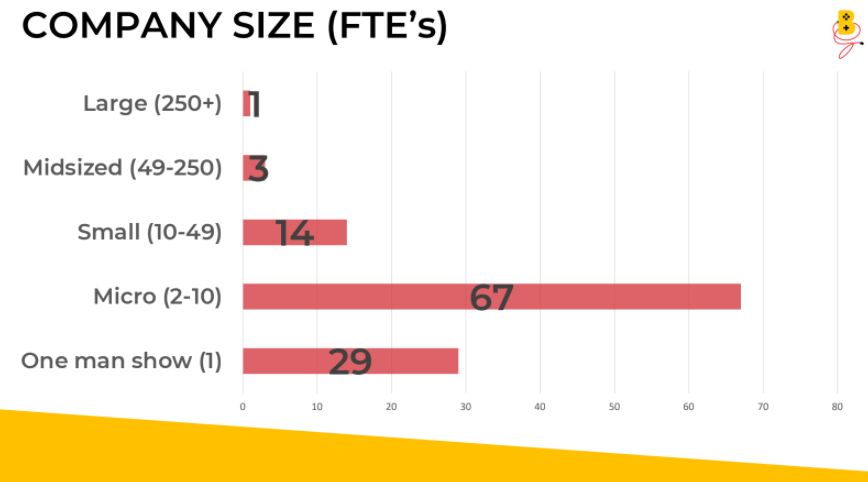

This doesn’t come as a surprise when looking at the size of our local game companies. Over 84% of companies employ between 1-10 people, and as much as 25% are one-man shows. Dealing with high wage costs and limited budgets makes it difficult for Belgian game companies to properly scale. A small uptick is that 42% of companies expected to see their FTE count rise in 2020, and that 43% have been in business for more than 5 years. Yet, it seems clear that there’s a need for more support if we want to get another Belgian game company at the juggernaut level of Larian Studios.

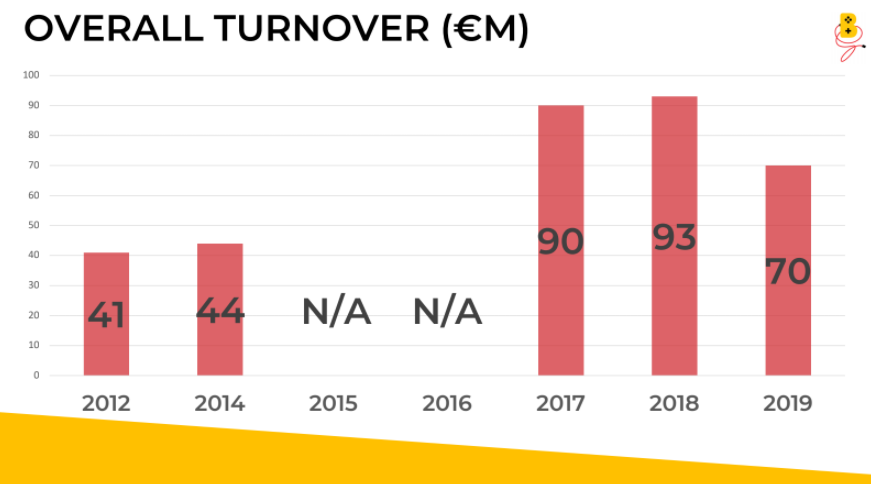

Is that really necessary? Well, looking at the overall turnover, down to € 70 million compared to € 93 million last year, we’d argue it is. As the majority of this income is generated by Larian Studios, who haven’t released a new game in 2019, it’s quite logical total revenue is dwindling. On the plus side, over half of participants say they expect their turnover to grow in 2020, and the results of Baldur’s Gate 3 Early Access Steam launch last September will make sure this number picks up again for the year 2020. But wouldn’t it be nice to have one or two bigger Belgian players that are able to soften the blow as long as Larian’s in between releases?

Our General Manager, David Verbruggen, puts it this way: “We are very happy to welcome more companies in our local ecosystem, but for our sector to grow to the next level, we need to significantly boost investment and job creation. This in turn will lead to more and bigger hits, feeding into our ecosystem to make it larger, healthier and more robust.”

The only way to do that is give our companies more support to grow and expand. Tax shelter could be part of the solution for this problem and a lot of companies are still anxiously awaiting more news. Over half of our game studios says they’re looking at tax shelter to fund future projects, while 44% says it’s too early to tell.

Other results are in the same vein of last year. Over half of our game companies identify as a game studio. The majority (58%) of the games being built are entertainment games, with serious games following at almost 23%. Artistic games and educational each make up a little under 10% of all games developed. On the platform side pc, VR, mobile and Nintendo Switch are the most profitable platforms. Finally, looking ahead, 20% of studios is planning to release a game on one or more next gen consoles.